Taxing billionaires has become one of the most politically appealing ideas in American politics. As policymakers search for new ways to finance expanding public spending, calls for a direct tax on accumulated wealth have moved from the margins of policy debate to the political mainstream. Nowhere is that shift more evident than in California, where a proposed ballot initiative would impose a one-time five percent tax on the wealth of the state’s billionaires.

On June 17, the proposal qualified for the November ballot after state officials verified the required petition signatures. If approved, supporters estimate the measure would raise roughly $100 billion for healthcare, education, and social programs. Yet sound economic policy should be judged not by its intentions but by its consequences. The real question is not whether billionaires can afford to pay more, but whether a wealth tax can generate the promised revenue without driving away the investment, entrepreneurship, and innovation that created that wealth in the first place.

Why Wealth Taxes Don’t Work

The appeal of a wealth tax is easy to understand. Asking a handful of billionaires to finance public spending may sound politically attractive, but history suggests the economics are far less convincing. Unlike income taxes, wealth taxes target accumulated assets—not annual earnings — including business equity, investments, real estate, and intellectual property. Because most billionaire wealth is invested in productive businesses rather than sitting idle in bank accounts, taxing it discourages investment, entrepreneurship, and innovation while encouraging capital to flow to more competitive jurisdictions.

International experience reinforces this point. An OECD report finds that wealth taxes discourage entrepreneurship and risk-taking, weakening innovation and long-term economic growth. These findings help explain why the number of countries levying wealth taxes fell from 12 in 1996 to just five today, as many governments abandoned them after they generated little revenue while imposing high economic and administrative costs. Even where they remain, they have historically raised only about 0.2 percent of GDP while discouraging investment and weakening long-term economic growth.

The existing tax burden makes this case even harder to justify. America’s wealthiest taxpayers already face one of the world’s most progressive tax systems, with a combined state, local, federal, and international tax rate of 59 percent. Recent research also found that US billionaires pay higher effective tax rates than their counterparts in the Netherlands, Sweden, Norway, and France and, contrary to the common narrative, pay the highest tax rates among all Americans. California is particularly vulnerable because it already relies heavily on a small number of high-income taxpayers to finance its budget.

The proposal is also exceptionally difficult to administer. Much of the wealth it targets — private businesses, artwork, intellectual property, and real estate — has no clear market value, making annual valuations costly, subjective, and prone to dispute. California would compound these challenges by imposing steep penalties on taxpayers and appraisers whose valuations differ from those of state authorities, increasing compliance costs and creating legal uncertainty for investors and entrepreneurs.

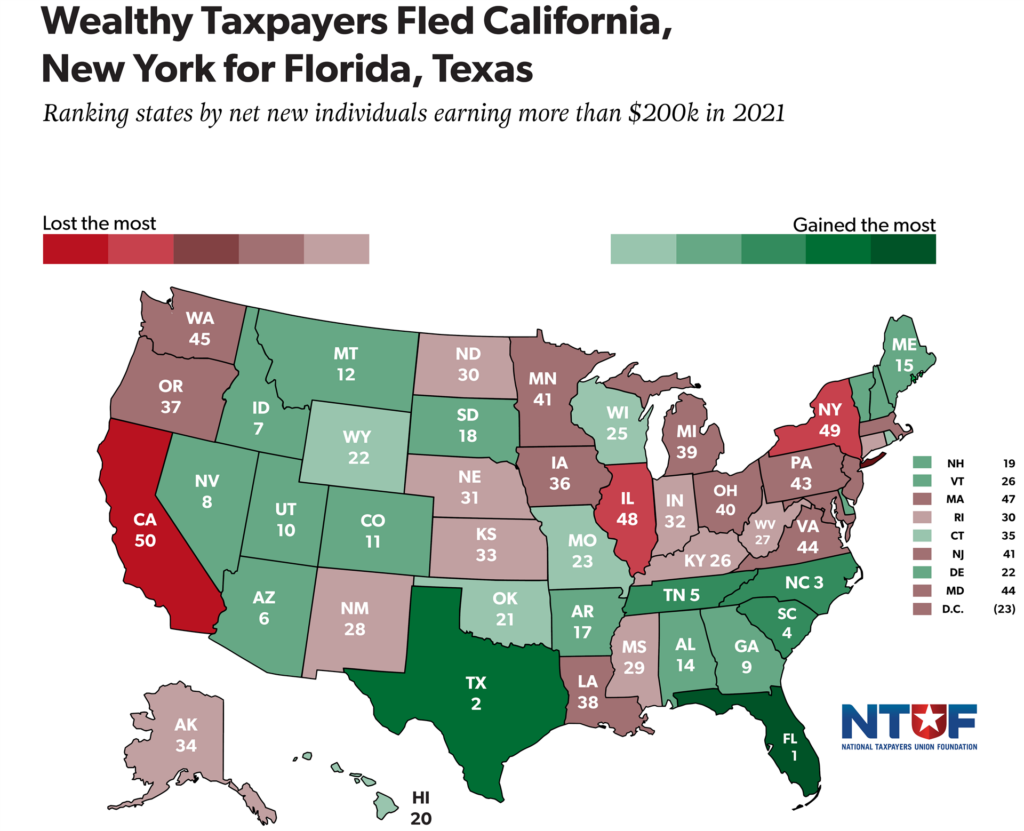

Finally, the proposal ignores a basic economic reality: capital is mobile. Before France repealed its wealth tax in 2018, an estimated 10,000 wealthy individuals with €35 billion in assets had already left the country. California is already experiencing a similar trend, losing more wealthy individuals to outmigration than any other state and recording a net loss of 1.6 million residents to interstate migration over the past decade. A wealth tax would likely accelerate that exodus, forcing some entrepreneurs whose wealth is tied up in their companies to sell shares or dilute ownership simply to pay the tax, weakening founder control, discouraging long-term investment, and undermining California’s position as a global center of innovation.

California’s Billionaire Tax Is Already Backfiring

If California’s billionaire tax is intended to raise the projected $100 billion from the state’s wealthiest residents, early evidence suggests it may already be backfiring. Even Governor Gavin Newsom, who opposes the proposal, has warned that it risks driving high-income taxpayers out of the state. Rather than waiting to see whether voters approve the measure, many of California’s wealthiest entrepreneurs and investors have already begun relocating to lower-tax states, shrinking the very tax base the proposal seeks to capture.

Among those reported to have left California or moved to lower-tax states are Google co-founders Larry Page and Sergey Brin, PayPal co-founder Peter Thiel, venture capitalist David Sacks, financier Don Hankey, and film producer Steven Spielberg. Meta founder Mark Zuckerberg has also reportedly acquired property in Florida. Their departures demonstrate that taxpayers often express their preferences with their feet as much as with their votes.

The fiscal outlook is even bleaker than supporters anticipate. A Stanford University Hoover Institution study estimates the proposal would raise only about $40 billion, not the promised $100 billion, after accounting for billionaire departures and correcting flaws in its revenue projections. It also finds that just six publicly confirmed departures removed roughly $536 billion — nearly 30 percent of the proposed tax base — leaving the measure with a projected net fiscal loss of about $25 billion once future income tax losses are included.

Even if voters reject the measure, the damage may not end there. Investors and entrepreneurs respond not only to enacted policies but also to the broader political climate, and the prospect of recurring wealth taxes could discourage long-term investment, startup formation, and business expansion while encouraging more high-income residents to relocate.

California’s proposal reinforces a lesson repeatedly demonstrated around the world: wealth taxes rarely fail because taxpayers refuse to pay—they fail because taxpayers adapt. In an increasingly mobile economy, governments cannot assume that capital will remain in place as tax burdens rise. By the time Californians vote in November, much of the wealth the proposal seeks to tax may already have left the state, taking investment, jobs, innovation, and future tax revenue with it.