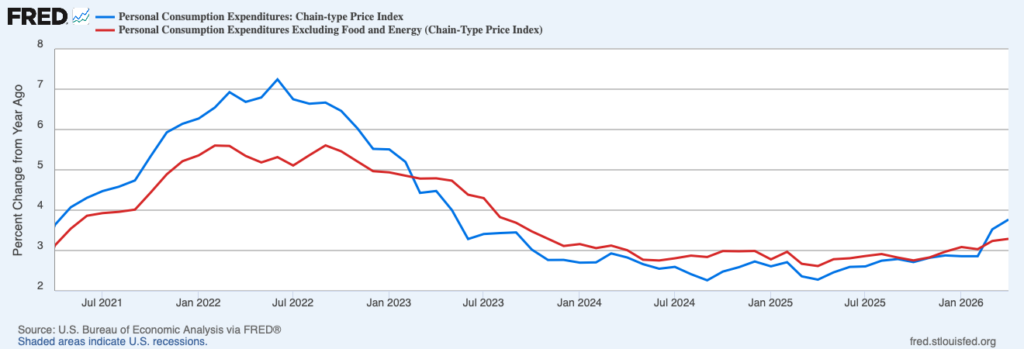

The conflict in the Middle East has pushed prices higher this year. But the latest data from the Bureau of Economic Analysis suggests the worst of the price hikes may be in the rear-view mirror. The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at an annualized rate of 4.9 percent in April 2026, down from 8.3 percent in the prior month. The PCEPI grew at an annualized rate of 4.8 percent over the last six months and 3.8 percent over the last year.

Figure 1. Headline and Core Personal Consumption Expenditures Price Index Inflation, April 2021 – April 2026

Core inflation, which excludes food and energy prices and is thought to be a better gauge of the underlying rate of inflation, also declined. Core PCEPI grew at an annualized rate of 2.9 percent in April 2026, down from 3.6 in the prior month. It grew at an annualized rate of 3.8 percent over the last six months and 3.3 percent over the last year.

Although inflation has declined on a month-over-month basis, the year-over-year rate has ticked up. Headline PCEPI inflation climbed from 3.5 percent to 3.8 percent, whereas core PCEPI inflation increased from 3.2 percent to 3.3 percent. What — if anything — the Fed should do about the higher inflation depends in large part on why inflation is above target.

The pass-through from energy prices to everything else certainly explains a portion of the difference between inflation and the Fed’s two-percent target, and the Fed should not respond to that portion. When constrained supplies — of energy, or anything else — push prices higher, those higher prices help individuals make appropriate decisions about whether and how much of the more-scarce item to buy. Unless the Fed has a secret stash of oil, natural gas, or fertilizer lying around, it won’t be able to improve matters on that front.

Constrained supplies cannot explain all of the difference between inflation and the Fed’s target, however. Some of the excess inflation is due to excess nominal spending. When the amount of money being spent in an economy grows faster than the real value of goods and services being produced, prices must rise. And when nominal spending growth outpaces real output growth, prices rise more rapidly. Hence, a surge in nominal spending growth results in higher inflation. To improve matters, the Fed can bring nominal spending growth back down to a rate consistent with its inflation target and the expected growth rate of real output.

Over the five years preceding he pandemic, nominal spending grew around 4.1 percent per year. Loose monetary policy allowed nominal spending growth to surge from 4.3 percent for the year ending 2021:Q1 to 11.3 percent for the year ending 2022:Q1. Then, as the Fed tightened monetary policy, nominal spending growth declined. Nominal spending grew 7.8 percent, 5.5 percent, and 4.6 percent over the three years that followed. As nominal spending growth declined, so too did inflation. Over the 12 months ending in April 2025, PCEPI inflation was just 2.3 percent.

Alas, that disinflationary process has not merely stalled, but reversed. Nominal spending grew 5.9 percent from 2025:Q1 to 2026:Q1. And, with more money chasing after the same amount of goods, higher nominal spending growth has brought higher inflation.

It is tempting to attribute the increase in inflation to the salient supply shocks we have experienced over the last year or so, including the tariffs levied last year and the conflict in the Middle East beginning earlier this year. But here’s the thing: constrained supplies do not push nominal spending growth higher. Rather, faster nominal spending growth is the telltale sign of a demand-side problem.

Unfortunately, Fed officials do not appear to see it that way. As the minutes from the Federal Open Market Committee (FOMC) meeting held in April reveal, FOMC members attribute the higher inflation to the conflict in the Middle East, tariffs, and other supply-side factors:

Participants observed that overall inflation had moved up, in part because of recent global energy price increases, and remained above the Committee’s two percent longer-run goal. Participants generally noted that core inflation had also moved further above two percent. Several participants noted that the rate of increase in core goods prices remained elevated, at least in part reflecting the effects of tariffs. Some participants observed that higher fuel prices had caused a number of other prices to increase, including shipping costs and airfares. In addition to energy price increases, several participants noted that supply disruptions associated with the conflict in the Middle East had caused prices for fertilizer and some other non-energy commodities to rise. Some participants noted that recent price increases in the information technology sector had contributed to higher inflation. A few of these participants remarked that, while price increases in the software category were contributing meaningfully to the increase in core inflation, price increases in that category may not be good predictors of future overall inflation.

Furthermore, they “anticipated that high energy prices would continue to put upward pressure on overall inflation” and “generally expected that the effects of tariffs on core goods inflation would diminish over the course of this year” so long as tariff rates are not “increased above present levels, leading to additional upward pressure on inflation.”

It is somewhat odd that FOMC members did not explicitly acknowledge that excess demand has also pushed up inflation. At the meeting, members “generally observed that economic activity appeared to be expanding at a solid pace” and “generally anticipated that the pace of real GDP growth would remain solid this year.” Those observations are inconsistent with a supply-driven inflation story, wherein prices rise more rapidly as real output growth slows.

FOMC members even identified specific sources of demand at the meeting, noting “that business fixed investment remained robust, largely reflecting strength in the technology sector” and that “high levels of household wealth and fiscal policy” had supported consumer spending. They just did not connect the dots from robust demand to higher inflation.

There is a silver lining, however. Despite suggesting inflation is largely supply-driven, which would not typically warrant a monetary policy response, FOMC members thought the situation “could necessitate maintaining the current policy stance for longer than previously anticipated.” That change in the projected path of monetary policy amounts to a modest tightening, though probably not enough to meaningfully slow nominal spending growth. Moreover, a “majority of participants” agreed “that some policy firming would likely become appropriate if inflation were to continue to run persistently above two percent.” The Fed may tighten monetary policy further, and reduce nominal spending growth as a consequence, without ever acknowledging the demand-side problem.

Ideally, policymakers will implement the right policies for the right reasons. Barring that, however, I would certainly prefer they implement the right policies for the wrong reasons than implement the wrong policies. There is a risk that, by not fully understanding the situation, Fed officials will not react as they should to incoming data. But at least they are headed in the right direction.