For decades, a small group of oil-producing states has exercised extraordinary influence over the global economy—not through innovation or competition, but through coordinated supply restriction. The Organization of the Petroleum Exporting Countries (OPEC) has long operated as one of the world’s most powerful cartels, managing oil supply to sustain higher prices and shape global energy markets. In a competitive market, producers expand output, compete, and innovate. Cartels do the opposite: they restrict supply, distort prices, and impede the natural functioning of markets.

That system is now beginning to crack. On May 1, 2026, the United Arab Emirates, one of OPEC’s largest and most strategically important producers and a member since 1967, withdrew from the organization, citing “national interests” and a desire for an independent energy policy, thereby removing 10 to 15 percent of the cartel’s production capacity.

This departure is part of a broader trend: Qatar and Ecuador left in 2019, Angola followed in 2024, and countries such as Gabon and Indonesia have also stepped away. What once appeared to be a cohesive bloc is increasingly fragmenting, a sign that the cartel model itself is becoming harder to sustain.

The Economic Case Against OPEC

OPEC, founded in 1960, remains one of the clearest examples of cartel behavior in the modern global economy. Controlling roughly 40 percent of global oil production and around 80 percent of proven reserves, its members coordinate production quotas to restrict supply and sustain higher prices rather than allowing markets to adjust through competition.

Since the 1970s, the United States has frequently viewed OPEC as both an economic and geopolitical challenge, with presidents from Richard Nixon to Joe Biden criticizing the cartel for driving up energy costs and fueling inflation. President Donald Trump openly described OPEC as a monopoly, while Congress has repeatedly considered antitrust measures against the cartel.

One of the clearest examples of OPEC’s market distortion is its deliberate supply restriction despite soaring global demand. Between the end of World War II and 1973, oil production in future OPEC countries rose from roughly 3 million to 30 million barrels per day, supporting one of the strongest periods of economic growth in modern history. Yet despite global oil demand rising after the 1973 oil crisis to nearly 90 million by 2012, OPEC repeatedly kept its production ceiling near 1973 levels, around 30 million barrels per day, to sustain higher prices. It is therefore unsurprising that economic research generally concludes that oil prices would likely be lower in the absence of OPEC’s coordinated supply restrictions.

The effects of this policy extend far beyond the oil sector. Because oil is essential to transportation, manufacturing, agriculture, and global trade, OPEC’s supply restrictions raise costs across the entire economy. According to IMF estimates, each sustained 10 percent increase in oil prices can raise global inflation by about 0.4 percent while reducing global economic output by around 0.1–0.2 percent.

Higher energy prices fuel inflation, weaken purchasing power, and disproportionately harm lower-income households and energy-importing developing countries. In 2022, for example, Pakistan’s oil import bill more than doubled, contributing to a severe foreign exchange crisis that required IMF intervention.

Beyond these immediate effects, academic research has also highlighted the cartel’s broader structural inefficiencies. A major study by researchers at Duke University, the University of California, Los Angeles, and KU Leuven found that OPEC’s production restrictions increased global oil production costs by roughly $160 billion and shifted investment toward more expensive extraction methods such as offshore drilling and fracking. By limiting low-cost production, the cartel distorted investment decisions, reduced market efficiency, and imposed substantial costs on the global economy.

Why OPEC Is Becoming Increasingly Unsustainable

Despite its historical influence, OPEC has always faced a fundamental problem: cartels are inherently unstable. Maintaining coordinated production cuts requires discipline, yet each member has an incentive to quietly exceed quotas and capture additional profit. As a result, quota violations, hidden discounts, and overproduction have been recurring features of OPEC since its founding, exposing the internal contradictions of a system built on collusion rather than competition.

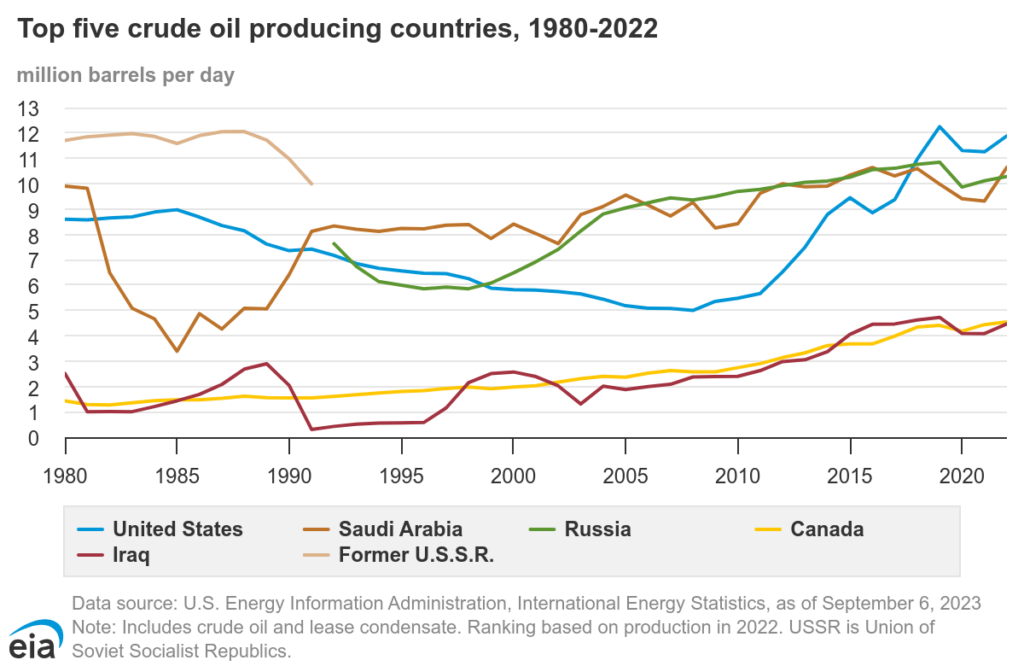

At the same time, external competition has steadily weakened the cartel’s power. The rise of non-OPEC producers — especially the United States shale industry — dramatically increased global supply and reduced OPEC’s ability to control prices. Between 2008 and 2025, US shale production surged from roughly 5 million barrels per day to 13.7 million barrels per day, helping turn the US into the world’s largest oil producer. This wave of competitive production contributed to the sharp collapse in oil prices in 2014–2016 and significantly reduced OPEC’s market share and pricing power.

Ironically, OPEC’s own strategy helped create the forces weakening it. Years of artificially high oil prices incentivized investment in technologies such as hydraulic fracturing and horizontal drilling, fueling the US shale revolution. By 2014, OPEC was forced to abandon its price-support strategy and flood the market in an unsuccessful attempt to crush US shale producers. Yet technological innovation, growing competition, and expanding investment in alternative energy continue to erode the cartel’s long-term power, demonstrating a broader economic reality: when markets are free to respond to price signals, competition and innovation eventually unravel cartel power.

This shift is increasingly visible even within OPEC itself. The United Arab Emirates’ departure reflects a growing recognition that competing freely may be more sustainable than remaining bound to restrictive quotas. As competition, innovation, and new energy sources continue to weaken cartel power, global energy markets are moving toward more open, market-driven production.

OPEC may still influence prices in the short term, but the broader trend is clear: market forces are gradually overtaking coordinated restriction.